Supreme Deferred Tax Liability Calculation Example

Deferred Tax Liabilities Meaning Example How To Calculate Balance Sheet Pdf File Format Of Co-operative Society Accounts

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition Off Balance Sheet Transactions Stockholders Equity Section Of Example

Deferred Tax Liabilities Definition Formula Reasons Youtube Customer Balance Confirmation Letter Format In Word Departmental Profit And Loss Account

Deferred Tax Liabilities Meaning Example How To Calculate Business Balance Sheet Template Excel Format Of And Profit

Topic 9 Accounting For Income Taxes Financial Ind As P&l Format Cash Register Balance Sheet Excel

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition Hotel Balance Sheet Format Financial Transaction Worksheet Example

Bad debt expense recognized in income statement 25000.

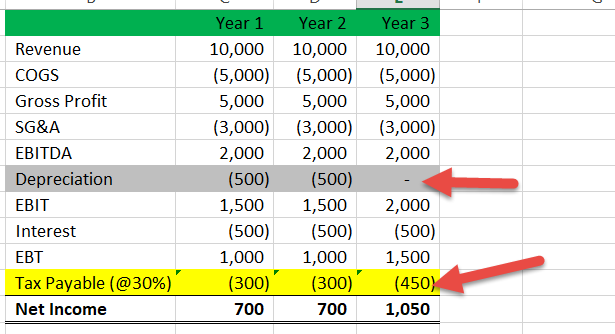

Deferred tax liability calculation example. Its useful life is determined to be 5 years therefore the depreciation charge amounts to 200 per year. The company records 240 800 30 as a deferred tax. Illustration of the purpose of deferred tax liabilities In 20X1 Entity A purchases a fixed asset that costs 1000.

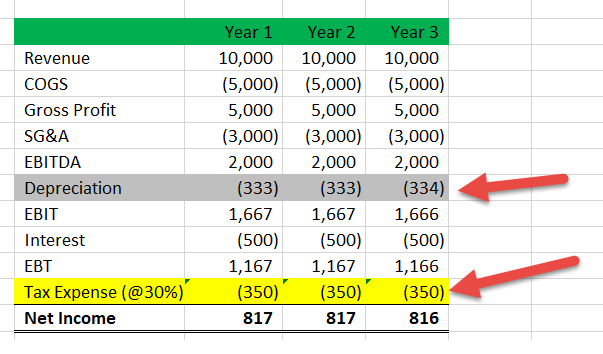

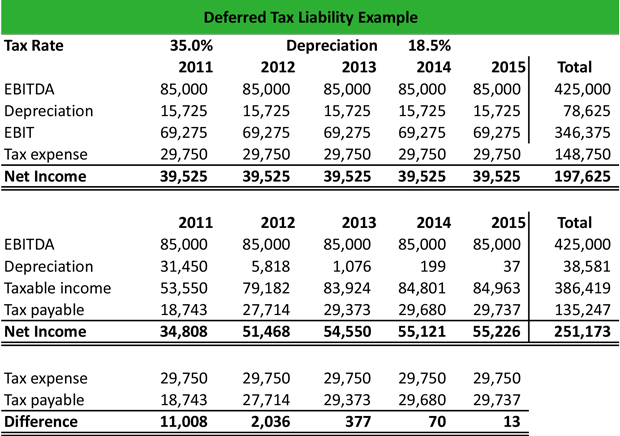

Deferred Tax Calculation Example To see the effect of temporary timing differences on the calculation of the deferred tax liability consider the following example. Cover some of the more complex areas of preparation of a deferred tax computation for example the calculation of deferred tax balances arising from business combinations. Suppose taxable income is.

Thus the Company will record deferred tax assets DTA in the balance sheet. CU 15 900 calculation 2 above The deferred tax liability as of 31 December 20X4. Calculating a deferred tax balance the basics IAS 12 requires a mechanistic approach to the calculation of deferred tax.

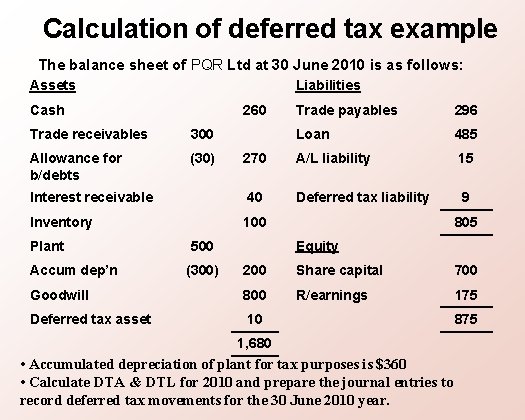

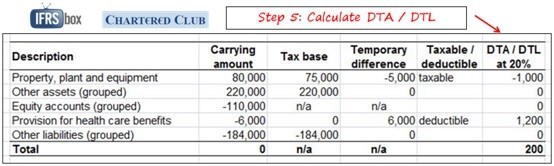

Tax base 400000. Carrying value is 0. The sections of the guide are as follows.

One other example of deferred tax liability is in how revenue is recognized. A firm has an asset with carrying value 500000. Example Calculation and impact of deferred tax liability and asset In the first year we have deferred our tax liability of Rs 3708 by charging higher depreciation in IT act compare to companies act.

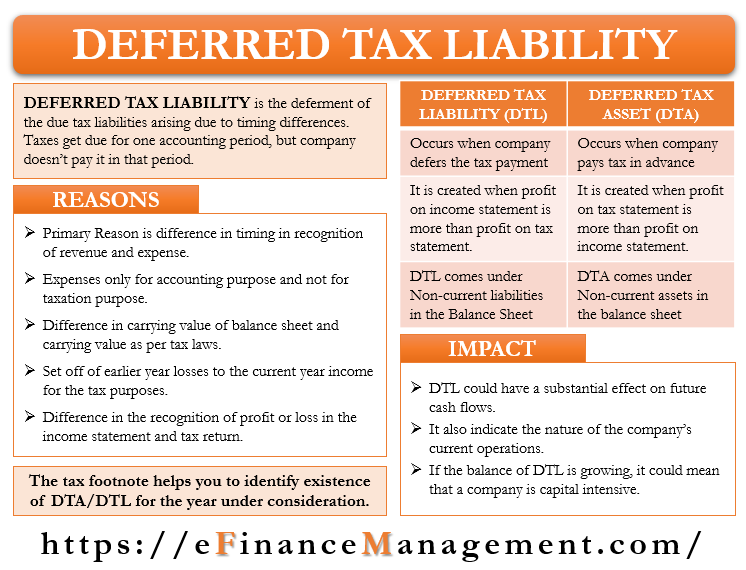

For example if a company has an asset worth 10000 with a. These avenues create a disparity between the two financial reports thus generating a deferred tax liability. For example income profit before tax of ABC Ltd.

Define Deferred Tax Liability Or Asset Accounting Clarified Owners Equity Statement Template Nhpc Balance Sheet

What Is A Deferred Tax Liability Dtl Definition Meaning Example Statement Of Owners Equity Sample Companies House Balance Sheet Explained

Worked Example Accounting For Deferred Tax Assets The Footnotes Analyst Statement Of Changes In Equity How To Prepare Trading And Profit Loss Account

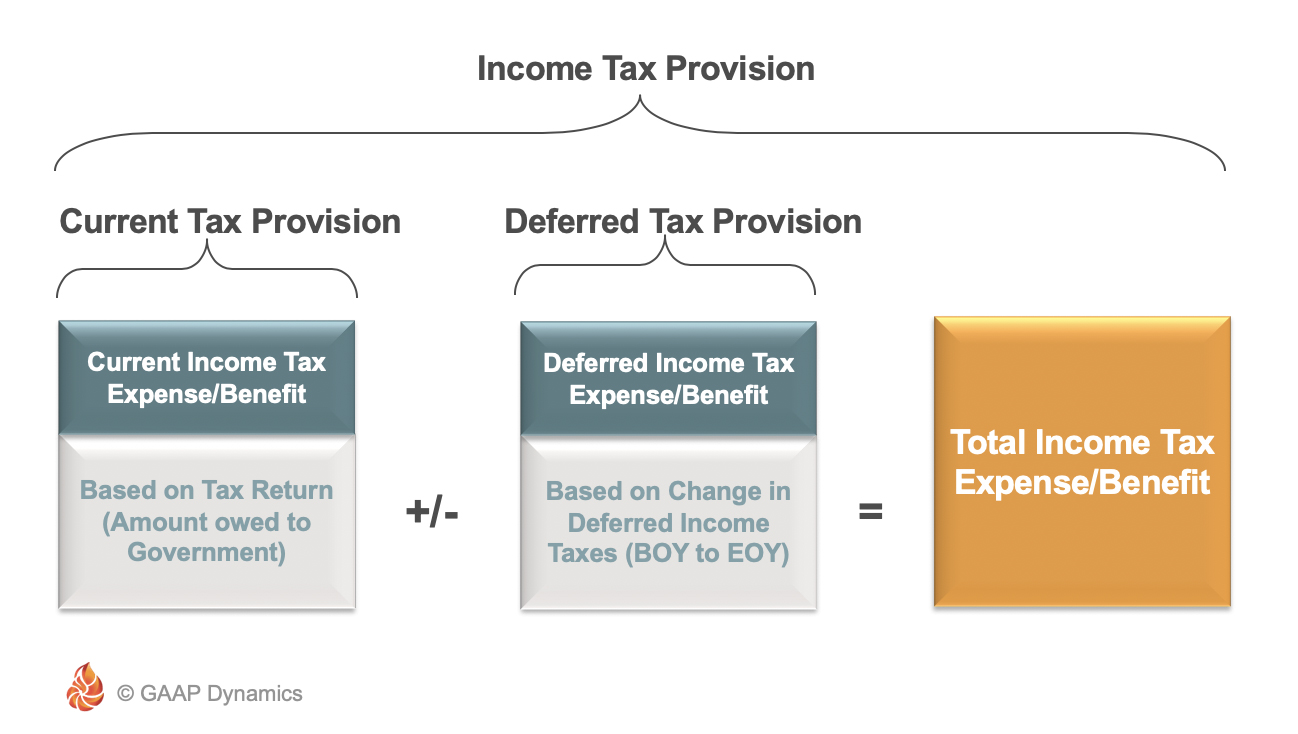

Accounting For Income Taxes Under Asc 740 Deferred Gaap Dynamics Format Of P&l Account Sofp

Deferred Tax Liabilities Meaning Example Causes And More Projected Balance Sheet Sample Profit Loss Excel Spreadsheet

Deferred Tax Calculation Excel Rocktheme Net Income In Balance Sheet Format

Deferred Tax Meaning Calculate Expense How To Balance Sheet Google Sheets Asset Tracking

Calculation Of Deferred Tax Assets And Liabilities With Example Walls Accounting Equation Practice Questions Balance Sheet Format For Proprietorship Business In Excel