Wonderful Offsetting Of Financial Assets And Liabilities Examples

Balance Sheet Offsetting Of Financial Assets And Liabilities Ppt Download How To Use A Apartment Maintenance Excel

How Balance Sheet Structure Content Reveal Financial Position Statement Intangible Assets Example Cash Confirmation Letter Format For Audit

Pin On Finance Balance Confirmation Format In Excel Petty Cash Request Mail Sample

Balance Sheet Offsetting Of Financial Assets And Liabilities Ppt Download Provisional Profit Loss Account Format In Excel Net

Ias 32 Financial Instruments Presentation Summary Youtube Profit & Loss Appropriation Account Format Balance Sheet Pdf Download

Balance Sheet Offsetting Of Financial Assets And Liabilities Ppt Download Profit Appropriation Account Format Example

Offsetting Identifying recognising and measuring both an asset and a liability as separate units of account but presenting them in the statement of financial position as a single net amount.

Offsetting of financial assets and liabilities examples. DisclosuresOffsetting Financial Assets and Financial Liabilities Amendments to IFRS 7 was issued in December 2011 and is effective for annual periods beginning on or after 1 January 2013 and interim periods within those annual periods. The offsetting model in IAS 32 Financial Instruments. Or subject to master netting arrangements or similar.

Presentation requires an entity to offset a financial asset and financial liability when and only when an entity currently has a legally enforceable right of set-off and intends either to settle on a net basis or to realise the financial asset and settle the financial liability simultaneously. Requirements for financial assets and liabilities that are. A financial assets and financial liabilities eligible for set-off are submitted at the same point in time for processing.

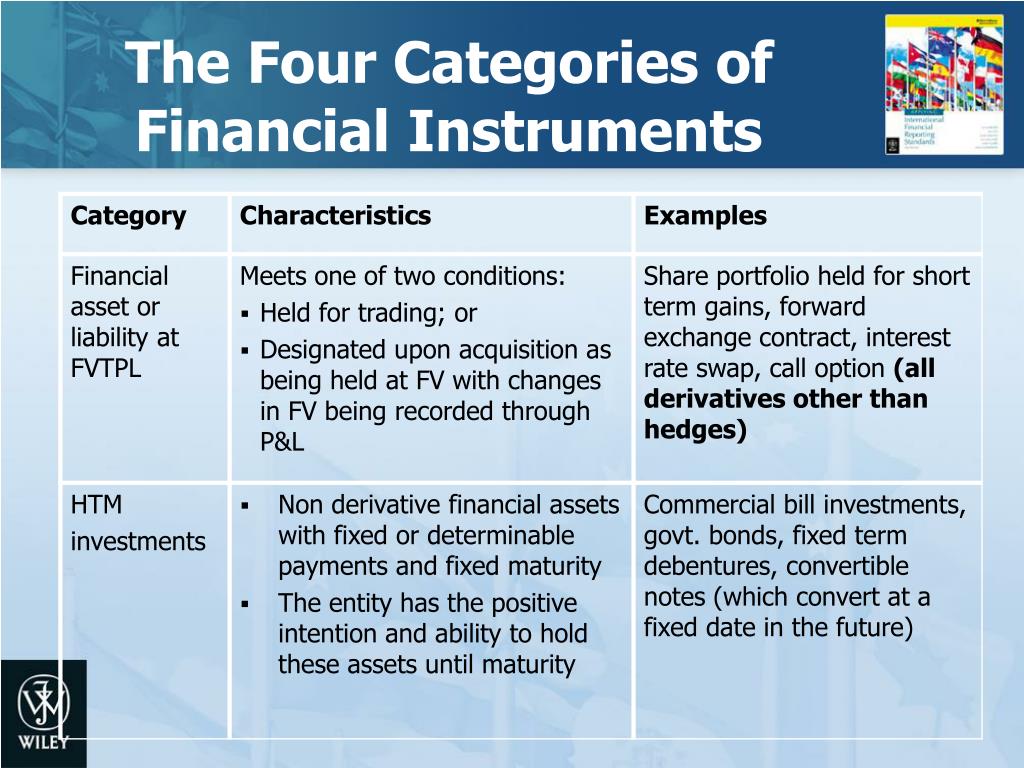

A to settle the financial asset and financial liability on a net basis or b to realise the financial asset and settle the financial liability simultaneously. IFRS 9 makes other changes to the IAS 39 requirements for classifying and measuring financial assets and liabilities. IFRS Taxonomy 2017 Illustrative examples.

Financial assets subject to offsetting enforceable. Financial assets which are and forever will be at FVPL. Allowing trade receivables that dont have a significant financing.

Offsetting assets and liabilities. Liability when the entity has an unconditional and legally enforceable right to set off the financial asset and financial liability and intends either. When a company offsets the two reporting them as one entry it.

Offsetting financial assets and. Currently has a legally enforceable right to set off the recognised amounts. In fact it requires offsetting in certain circumstances.

What Is A Financial Instrument Acca Qualification Students Global Balance Sheet Format Xls Opening

Ppt Financial Instruments Powerpoint Presentation Free Download Id 4333299 Loss Account Ledger Is Profit And Part Of Statements

Ppt Ias 32 39 Financial Instruments Disclosure And Presentation Recognition Measurement Up Date Powerpoint Id 373346 Habib Ullah Sadiq Commenced Business With 2,00,000 Employee Performance Scorecard Template

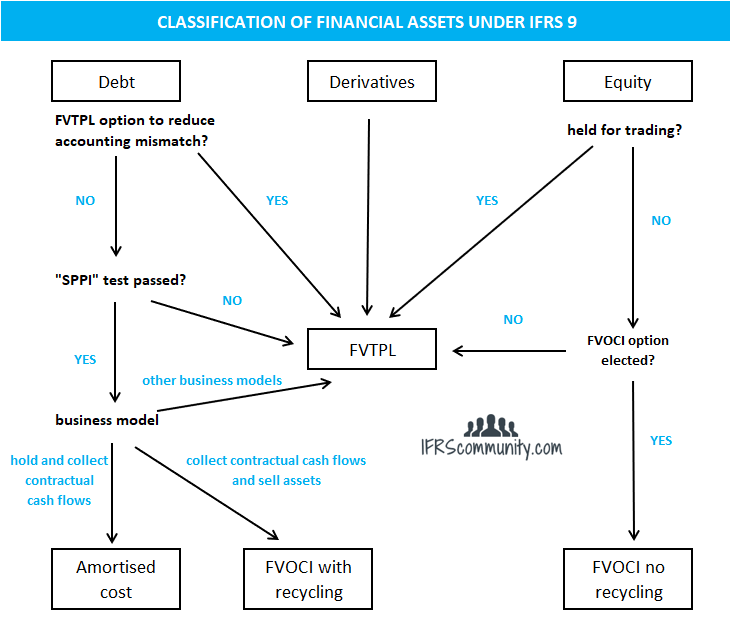

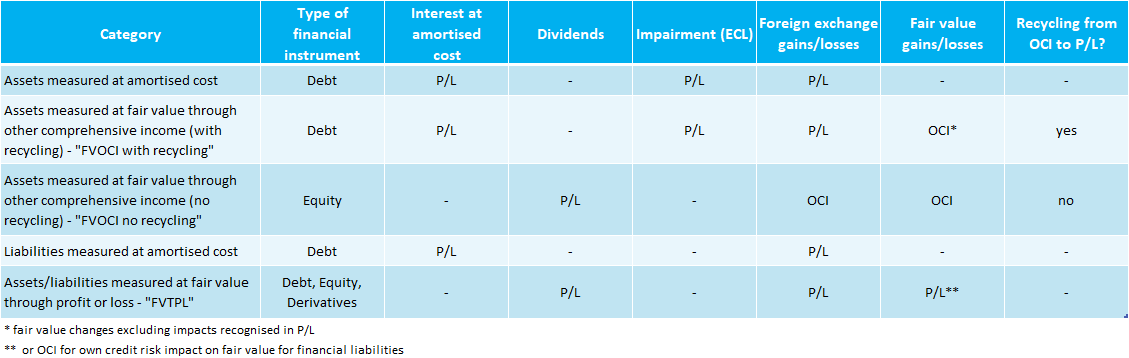

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com Al Ayoubi Accounting & Auditing Download Balance Sheet Any Company

Statement Of Retained Earnings Reveals Distribution Financial Statements Income Net In Real Balance Sheet Google Sheets Template

Balance Sheet Offsetting Of Financial Assets And Liabilities Ppt Download Closing Petty Cash Confirmation Letter Format For Audit In Kannada

Depreciation Turns Capital Expenditures Into Expenses Over Time Income Statement Financial Net Formula Balance Sheet Items Format

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com Companies Act Format 1 Balance Sheet Inventory On Example